A renewed M&A appetite

Turkey had a rather slow and volatile year of M&A and equity capital markets in 2016, but its performance in 2017 is certainly indicating a transition towards recovery and normalisation.

Turkish M&A Outlook

In 2016, M&A activity slowed in Turkey as a result of various political disturbances, such as a failed coup attempt, a referendum and terrorism, as well as a global decline caused by the uncertainty around the Trump administration, Brexit and the slowdown in China’s economic growth, among other things. Despite the loss of its “investable” grade according to the independent rating agencies, the Turkish M&A market has been showing strong signs of recovery in 2017. During this time, some conservative investors who could afford to put Turkey out of their radar temporarily did so while others showed their trust in Turkey’s long-term outlook through acquisitions. We expect the Turkish M&A activity to pick up further as investment banks launch their mandates that have been on hold due to the political instability and successful acquisitions and exits pave the way to normalisation.

So far, both strategic and financial investors have contributed to the M&A activity in 2017.

BRF, one of the largest poultry producers globally, and Vitol Group, a leading energy and commodities group, have respectively acquired Banvit, a leading Turkish poultry producer, and Petrol Ofisi, a leading Turkish gas and mineral oil distribution company with two important new strategic entrants. Another strategic player, BBVA, a globally leading bank, has reinstated its trust in its Turkish subsidiary, Garanti Bank, by acquiring a further 9.9 per cent stake.

Financial investors have also significantly contributed to Turkish M&A activity through acquisitions of targets in a variety of sectors, with logistics becoming the most eye-catching by attracting a number of financial investors.

In addition to the increased activity in the local M&A market, there has also been a significant interest of Turkish players investing or looking for opportunities in regions outside of Turkey trailing from the strength of the economic growth of the local market. Examples of such activities are Acıbadem Healthcare Group’s acquisition of two of Bulgaria’s biggest private hospital groups, City Clinic Group and Tokuda Group, and Vestel’s acquisition of Toshiba’s license to produce Toshiba TVs in Europe on an exclusive basis.

Negotiating and drafting legal documentation have also been affected by socio-political developments in Turkey: buyers have been trying to take a more risk-averse position to macro risks; however, they may still end up accepting such risks to make the transaction documents more attractive for the sellers. Moreover, sellers are making significant efforts to shorten the period between the signing and the closing of transactions as much as possible.

Turkish Equity Market Outlook

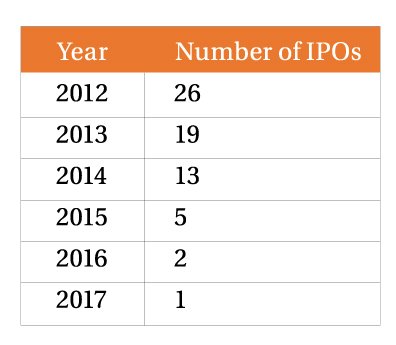

As of June 15, 2017, 404 companies are publicly traded on Borsa Istanbul. Historically, there have been periods of ups and downs in the number and volume of initial public offerings (“IPOs”) in Turkey, such as the IPO boom between 2004 and 2009 and the silent 2009 and 2010. However, from 2013, there has been a consistent slowdown in IPOs due to Turkey’s geographic position, and the ever-changing economic and political uncertainties. 2012 saw the highest number of IPOs, with 26 companies going public. 2013 was also a strong year due to the amendments to the Turkish Capital Markets Law, which aimed at increasing investor confidence. In 2014, the number of IPOs dipped, whereas global IPO numbers peaked until 2010. This negative affect weighed heavily upon the then-upcoming municipal, parliamentary and presidential elections in 2014 and 2015, and uncertainties preceding the elections became an obstacle in finalising IPO applications. As shown on the table below, the number of IPOs per year decreased drastically between 2012 and 2016.

Source: Turkish Capital Markets Board Data

This trend seems to be changing in 2017. Now that the political uncertainties have been left behind with the referendum in April 2017, and the Turkish lira is gaining strength against hard currencies, the deals started to follow one another. May witnessed the IPO of Global Ports Holding plc, which is Global Ports Holding’s UK subsidiary, on the London Stock Exchange. This was the first-ever IPO of a Turkish group on the London Stock Exchange. Mavi, the leading Turkish lifestyle fashion company, followed in June. The Mavi IPO on Borsa Istanbul was particularly important for several reasons. It was the first successful Turkish IPO in 2017, and is the largest IPO in dollar terms since 2013. It is the very first exit of a private equity investor through an IPO in Turkey, demonstrating to international private equity firms interested in Turkish assets that this exit strategy, frequently used in Europe, is also available to them in Turkey. It is also important that the first Turkish PE exit through an IPO happened while the PE exits through IPOs in Europe are declining.

These two deals showcase Turkey’s strong economic programs and the rising interest in Turkish capital markets. They promise to shake up a stagnating market for Turkish IPOs, characterised by years of cancelled or postponed sales. There are a number of other deals in the pipeline for the second half of 2017 and these two deals will encourage others as well.

Text by:

Eren Kurşun (MBA), partner, head of mergers & acquisitions and private equity, Esin Attorney Partnership

Muhsin Keskin, partner, head of capital markets and banking finance, Esin Attorney Partnership